ACQM Tactical Macro-Market Regime Risk Overlay

Institutional-Grade Macro & Market Risk Signals for Advisors Who Want Control — Not Outsourcing

Transform any Portfolio Into a Dynamic, Regime-Aware, Risk-Managed Solution

Most advisors want the benefits of institutional macro awareness without switching models or strategies, outsourcing investment decisions, or disrupting their investment philosophy.

The ACQM Tactical Macro-Market Regime Risk Overlay is a standalone macro-risk intelligence system that layers on top of any portfolio to help advisors navigate market regimes, manage risk with confidence, and make more consistent allocation decisions with a clear, data-driven framework.

You keep your models. You keep your philosophy. We give you the signals, structure, and clarity to elevate it.

What are Common Issues with Static Portfolios?

Markets do not move in straight lines.

They shift through:

Inflationary vs disinflationary regimes.

Expansion vs contraction.

Liquidity abundance vs tightening.

Risk-on vs risk-off sentiment cycles.

Yet most portfolios are constructed as if market conditions are static.

Advisors often struggle with:

➡️“Should we reduce equity exposure right now?”

➡️How to interpret macro noise vs structural regime change.

➡️“Which asset classes look strongest in this environment?”

➡️“Which factors are leading the market?”

➡️“Is now a risk-on or risk-off period?”

➡️How to justify tactical allocation decisions to clients.

➡️Emotional or reactive decision-making during volatility.

Without a structured framework, tactical decisions can become subjective, narrative-driven and inconsistent across time.

What are Current Available Options to Advisors?

Most advisors fall into one of three approaches:

A) Static Allocation - Strategic 60/40 or diversified ETF models, periodic rebalancing and minimal tactical adjustment. This approach comes with limitation in form of no formal regime awareness.

B) Outsource to TAMP / Model Marketplace - Adopt third-party models, delegate asset allocation decisions. Common Limitation: Loss of internal investment differentiation and process ownership.

C) Discretionary Tactical Calls - Reduce equity after volatility, increase risk when sentiment improves and follow macro commentary or strategist views without knowledge or research which can be compliance issue. This approach is often reactive and inconsistent without systematic structure.

What an Ideal Solution for Advisors look like?

An effective solution should:

✔ Provide objective regime identification

✔ Distinguish structural shifts from short-term noise.

✔ Offer asset-class and factor context.

✔ Support tactical decision-making without replacing the advisor’s philosophy.

✔ Integrate with existing portfolio models.

✔ Maintain advisor control and discretion.

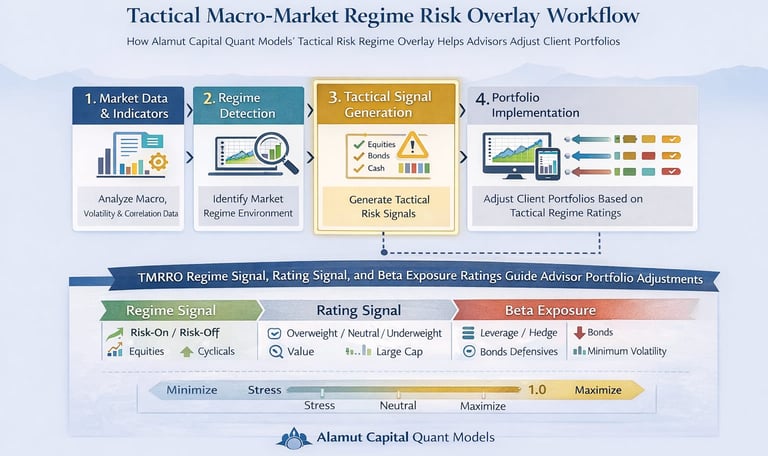

The ACQM Solution: TMRRO (Tactical Macro-Market Regime Risk Overlay.

A structured macro intelligence layer — not a portfolio replacement. Our overlay answers these questions with objective, data-driven signals, updated monthly.

Tactical Macro & Regime Risk Overlay (TMRRO) is a quantitative framework designed to identify and monitor evolving market regimes.

It provides:

✅Risk-on / Risk-off environment assessment.

✅Asset class relative regime ratings.

✅Factor leadership and rotation insights.

✅Structured tactical implementation guidance.

TMRRO does not replace your portfolios, It enhances them.

✔ It allows advisors to:

✔ Adjust exposures with discipline.

✔ Document and justify tactical shifts. This helps with Compliance reviews.

✔ Reduce emotional decision-making.

✔ Institutionalize investment process.

✔ Differentiate investment oversight.

How Advisors Benefit?

A CIO-quality macro framework at a fraction of the cost. Advisors use our overlay to:

✅ Improve risk-managed decision-making.

✅ Improve quality of low-cost index Portfolio Strategy.

✅ Support client narratives with data, not opinions.

✅ Reduce emotional/subjective allocation calls.

✅ Enhance investment process documentation.

✅ Demonstrate a more institutional approach to portfolio oversight.

✅ Advisors retain 100% branding.

✅ No AUM fees dragging Advisor's margins.

Who is TMRRO fit for?

TMRRO is built for Advisors who understands that compounding in investments is long-term but interruptions in compounding is recurring and is usually correlated to market regimes.

TMRRO is fit for you, if:

You want to discipline and process behind allocations decisions.

You want to use low-cost index ETF portfolios but also want to timely limit drawdowns.

You want to continue using your existing investment framework (Models, Philosophy, etc) but want risk minimization framework without hedging.

Contact Us

models_solution@acquantmodels.com

© 2026. All rights reserved.

Disclaimer: The model portfolio strategies provided by Alamut Capital Quant Models Inc. are offered solely to registered advisers and are licensed as intellectual property. We do not provide personalized investment advice, portfolio management services, or recommendations to any individual investor.

The information provided is not intended to be and does not constitute financial, legal, tax, or investment advice. Implementation of any model strategy is the sole responsibility of the subscribing advisor or portfolio manager, who must determine its suitability and compliance with their clients’ investment objectives, risk profiles, and regulatory obligations.

Alamut Capital Quant Models Inc. is not registered as an investment adviser in any jurisdiction and does not interact with any investors. The firm does not offer account-level services, make investment decisions on behalf of clients, or assume discretionary authority over assets.

Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. Use of our models does not guarantee any specific outcome or performance.

Alamut Capital Quant Models Inc

Get in touch with us to inquire about our Quantitative Investment Solutions and demo of our strategies

Kitchener, Ontario, Canada