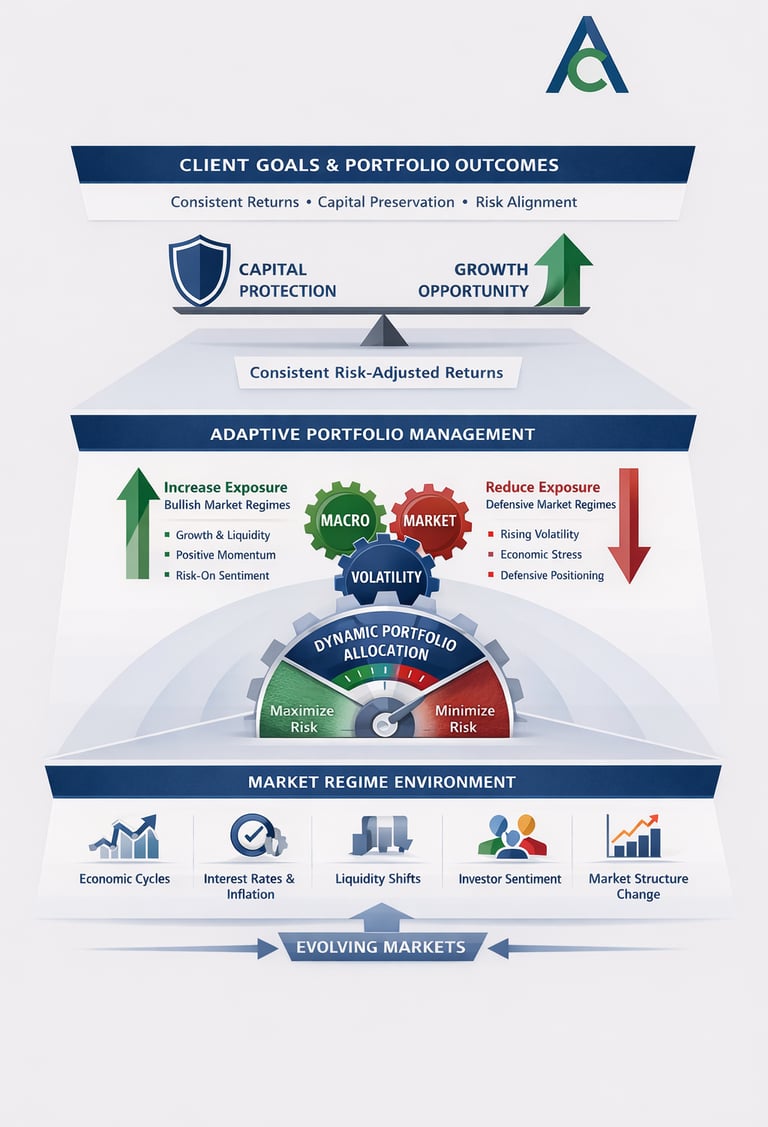

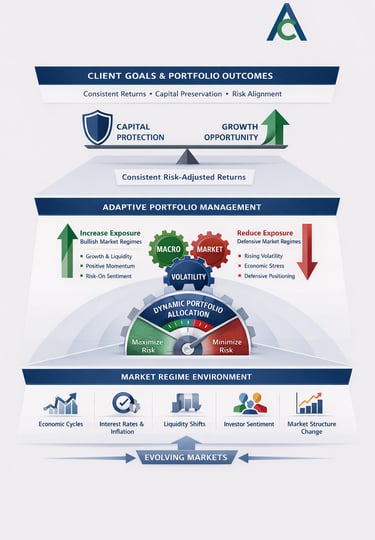

At Alamut Capital Quant Models, each strategy is built on the belief that successful investing requires balancing two equally important objectives: protecting capital during adverse market environments and capturing opportunities during favorable market conditions.

➡️ Financial Markets evolve through changing economic cycles, interest rate environments, liquidity shifts, and investor sentiment. Traditional static portfolio allocations often struggle when these conditions change. Our approach focuses on maintaining consistent outcomes by adapting portfolio positioning as market environments evolve rather than relying solely on fixed allocations or calendar-based rebalancing.

➡️ Portfolio allocation, the primary driver of long-term risk-adjusted returns is guided by our Macro, Market, and Volatility models. These models continuously evaluate economic trends, market momentum, and risk conditions to help determine when to increase participation, reduce exposure, or adjust risk positioning.

➡️ During periods when downside risks appear elevated, our strategies emphasize defensive positioning through diversification across uncorrelated exposures, volatility-aware allocation adjustments, and selective capital preservation techniques designed to help mitigate drawdowns and maintain portfolio stability.

➡️ When market risks rise, our strategies emphasize diversification, volatility-aware positioning, and capital preservation techniques designed to help reduce drawdowns. During constructive market environments, portfolios increase exposure to sectors, factors, and securities positioned to benefit from improving economic and market conditions.

➡️ Our quantitative and data-driven models help remove emotional decision-making while providing consistency and repeatability. The goal is to help advisors deliver smoother portfolio experiences and keep clients aligned with their long-term financial goals.

Our philosophy is designed to help advisors help clients stay invested and aligned with their long-term financial goals.

Investment Philosophy

Contact Us

models_solution@acquantmodels.com

© 2026. All rights reserved.

Disclaimer: The model portfolio strategies provided by Alamut Capital Quant Models Inc. are offered solely to registered advisers and are licensed as intellectual property. We do not provide personalized investment advice, portfolio management services, or recommendations to any individual investor.

The information provided is not intended to be and does not constitute financial, legal, tax, or investment advice. Implementation of any model strategy is the sole responsibility of the subscribing advisor or portfolio manager, who must determine its suitability and compliance with their clients’ investment objectives, risk profiles, and regulatory obligations.

Alamut Capital Quant Models Inc. is not registered as an investment adviser in any jurisdiction and does not interact with any investors. The firm does not offer account-level services, make investment decisions on behalf of clients, or assume discretionary authority over assets.

Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. Use of our models does not guarantee any specific outcome or performance.

Alamut Capital Quant Models Inc

Get in touch with us to inquire about our Quantitative Investment Solutions and demo of our strategies

Kitchener, Ontario, Canada